-

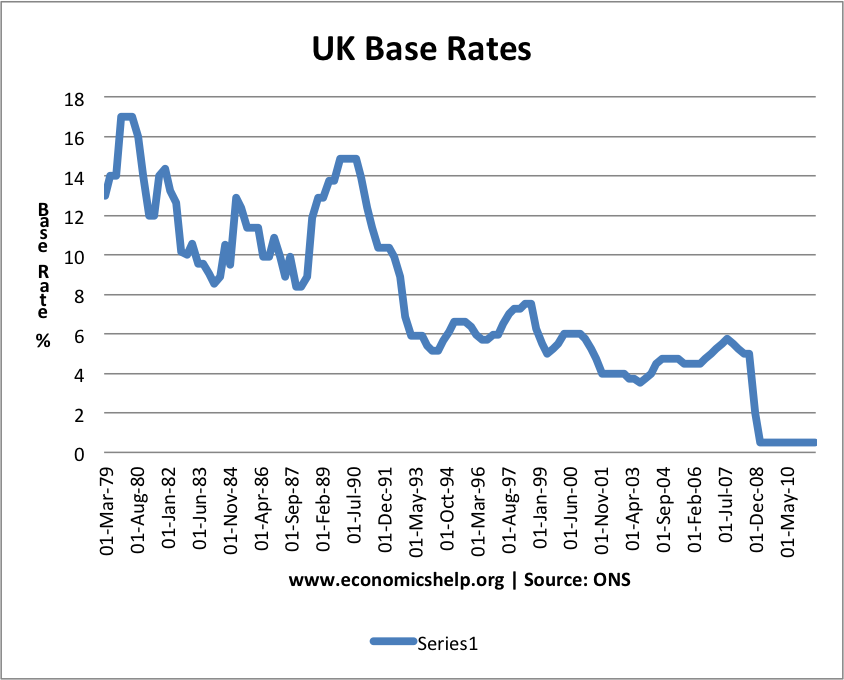

The end of our five-year fixed mortgage is in sight and looking to lock in a good deal. We have a small LTV (<20% I think). Not sure whether to get another fix or get a tracker. @Hefty - you know about these things in our 'hood...

-

Talk to Neezam - http://www.themortgagebroker.co.uk/member/neezam-romjon

-

I was discussing this with a mate at work. The conclusion was that if you can predict property price changes, interest rates and the rest in this current climate then you can probably make enough money that you don't need a mortgage.

(I'd go fixed, probably a 5 year for security. My mate's theory was a 2 year, at which point you'll be able to get a better 5 year as property prices will have risen and interest rates won't as they'll all kick off in 2019 post-actual-Brexit. Who knows.)

-

My inclination is a 5-year fix, given the insanely low rates and potential for worldwide turmoil; but I have heard your mate's thoughts from a friend, also. Historically we've lost out by being on 5-year fixes, but that's because we bought our first place in 2006 - just before the crash. Guess it could go either way still, but ultimately we'd be better off paying a bit over the odds rather than 'oh shit' loads.

-

I'll be getting another 2 year fix in the spring, and then a 5 year deal thereafter.

Don't be scared about rates going up. If they do, it'll only be by a small bit, and it'll probably be leaked well in advance .

-

Does anyone recommend a particular one of those mortgages where you can offset savings and get them out again? Could it be worth trying to change mortgage sooner than the end of a fixed (couple years away)

Scenario is that we both have savings that we'd like to put towards overpaying, reducing interest and debt, and neither of us are clever investors. However, we're not overpaying because at some point one of us will probably want to take on the whole mortgage and we'll need the savings. I think. But it seems madness not to be reducing debt while we can. -

We offset with YBS, they seem to have the best rates for fixed offset. I've always been happy with our interactions with them. In fact they were amazing when Brexit happened six days before our completion and we worked with them to switch from 2 year to 5 year fixed.

Our reason for offset is that a self employed income means that the tax money that is saved over the year can contribute to the mortgage until it gets handed to hmrc.

-

Anyone know how long it takes to hear back from the valuer? The property that we're buying is being valued today by Colleys (through the Lloyd's group) and keen to understand the time frames involved. Anyone had any experience with Colleys? It's just the basic type 1 valuation I think.

-

I'm still dithering over what blinds to get. Thinking now of going for a roller blind for the bedroom. It's a very large window. My concern is whether I'd be bothered not being able to regulate the light (it's either up or down). Also, do these guys look reasonable (any experience of them)?

-

OT/WANTED: mrs_com works with vulnerable and at risk young people. One of the people she has been working with has just, after a year of being in and out of hostels/refuges, been allocated her own flat.

This is awesome (for many and varied reasons) but it is currently unfurnished and after arranging her deposit and paying off the (much more expensive) hostel place they have about £15 left.

Does anyone have any furniture or appliances they are looking to get rid off for free or in exchange for services provided by myself?

I believe she needs everything from a kettle to a bed. mrs_com is pursuing other resources obviously but if anyone needs rid of something in decent or serviceable knick, let me know.

The flat is in Islington and I do not have a car so local stuff appreciated but depending on need/offer I will work out how to get stuff moved around.

Any offer is appreciated.

Timmy2wheels

Timmy2wheels Hefty

Hefty deleted

deleted Howard

Howard aggi

aggi

princeperch

princeperch hoefla

hoefla mashton

mashton Soul

Soul dwl

dwl chris0

chris0 stevo_com

stevo_com Dammit

Dammit Aroogah

AroogahAbout

Owning your own home

Posted by

@Hobo

@Hobo

at the moment it is somewhere to live. back in 1997, it was a pragmatic decision as well.

we were living in one room sub let of a housing association place in Chalk Farm.

walthamstow was cheap. I knew the area a little. we needed somewhere to live. we bought somewhere to live.

if only it were that simple for people now...